Product

Introducing Rutter Embedded ERP

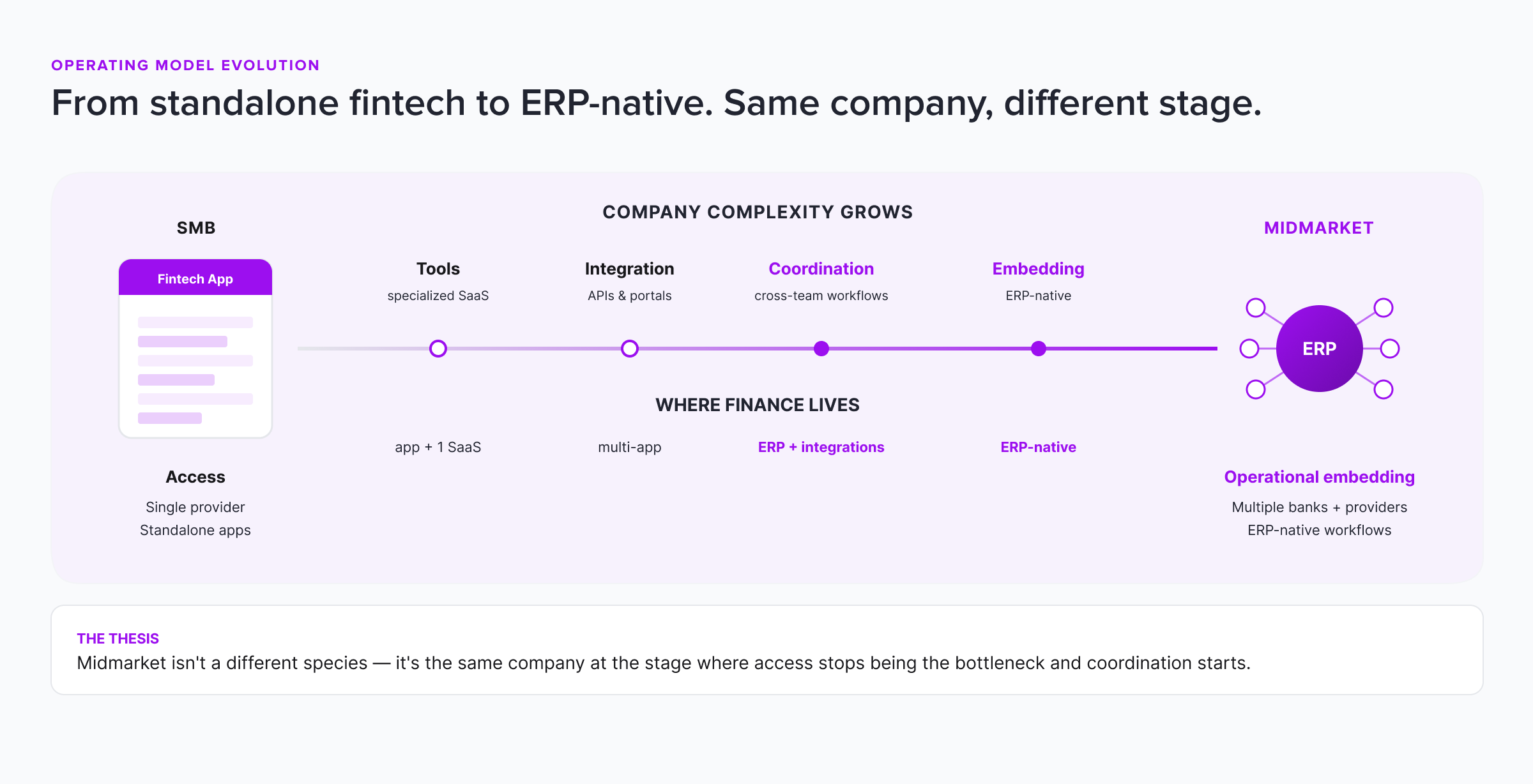

Rutter Embedded ERP is a new way for fintechs and banks to deliver their products as native experiences inside the ERPs their midmarket customers run on.

The first generation of fintech transformed financial access. Faster onboarding, self-serve tools, embedded finance, modern APIs, digital banking experiences. For SMBs, this shift was transformational. Small businesses could finally manage payments, treasury, expense management, lending, cash flow, and financial operations through modern platforms instead of fragmented legacy banking.

That model still works at the SMB end of the market. Mercury, PayPal, Airwallex, and Square are where SMBs run their financial lives.

When businesses move upmarket, operational complexity changes, and the Financial OS moves with it.

Midmarket finance teams operate differently from SMBs. Workflows become cross-functional:

Finance is no longer about access to financial tools. It's about coordination. That's why the ERP becomes strategically important. NetSuite, Microsoft Dynamics, Sage Intacct, Workday, SAP, and other ERPs are where midmarket controllers, treasury teams, and AP teams actually work. The ERP coordinates payments, approvals, treasury, reconciliation, procurement, AP/AR, financial reporting, and cash management. The ERP becomes the Financial OS.

Finance teams have wanted financial workflows inside their ERPs for as long as midmarket businesses have run on NetSuite, Dynamics, Sage, and Workday. The demand isn't new. What's new is that fintechs and banks now have rails worth embedding — real-time FX, instant payouts, modern card APIs, programmatic banking — and the infrastructure to embed them at scale is finally available.

Standalone financial portals still work for SMB use cases. For midmarket finance teams, they create friction. A controller reconciling card spend inside Dynamics doesn't want reconciliation workflows split across the ERP, banking portals, spreadsheets, and AP systems. Every context switch is operational overhead. This is why connectivity alone is no longer enough.

The market is moving from connected financial products to operationally embedded financial workflows. The first phase of embedded finance focused on embedding financial products into SaaS applications. The next phase is moving into systems of record.

The best financial products no longer connect to ERPs. They operate inside them. APIs move data. ERP-native workflows move operations.

Every ERP ecosystem brings its own SDK, authentication model, permissions system, deployment requirements, workflow structures, approval frameworks, and UI extension model. Treasury workflows inside Dynamics work nothing like AP workflows inside NetSuite or reconciliation inside Sage Intacct.

Most fintechs and banks underestimate how hard this is at scale. The result is slow internal projects, brittle one-off deployments, and limited ERP coverage.

We've spent the past five years building integration infrastructure across these ERP ecosystems with the leading banks and fintechs. The operational complexity is real.

The next generation of financial infrastructure won't be defined by APIs and connectivity. It will be defined by how deeply financial products embed into operational workflows. The first generation of fintech digitized financial access. The next generation will operationalize finance inside the systems of record midmarket customers run on.

Midmarket isn't a different species. It's the same company at the stage where access stops being the bottleneck and coordination starts. The fintechs and banks we work with that win this shift will be the ones capable of bringing modern financial rails directly into the ERPs where midmarket finance teams operate:

―――

Meeting your customer where they actually work isn't a feature. It's a market shift, and the fintechs and banks already moving on it are pulling ahead.

We just launched Rutter Embedded ERP for exactly this. We build native financial experiences inside your customers' ERPs, powered by your APIs.

Building integrated products is hard. We can do that together. Let's chat.